Market Update for the Month Ending August 31, 2014

Presented by Manning Wealth Management

U.S. markets shoot higher

August was another very strong month for U.S. stock markets. The S&P 500 Index closed the month up 4 percent, the Dow Jones Industrial Average up 3.6 percent, and the Nasdaq up 4.82 percent.

Fundamentals continued to strengthen. With 99 percent of companies reporting by the end of August, per FactSet, almost three-quarters had beaten earnings expectations and almost two-thirds had beaten sales estimates. The overall earnings growth rate was 7.7 percent.

Technicals remained strong following a strong bounce off of moving-average support levels early in August. All three major indices are now above their support levels.

Developed international markets suffered from political and economic problems and declined in August, with the MSCI EAFE Index down 0.15 percent. Technically, developed foreign markets continued to be weak.

On the other hand, emerging markets, as represented by the MSCI Emerging Markets Index, had a positive month, gaining 2.07 percent for August. Possible reasons include the growing likelihood of quantitative easing by the European Central Bank (ECB) and renewed growth in China. Technical signs for emerging markets are positive and improving.

Fixed income also showed gains in August, as rates declined. The 10-year Treasury rate continued to drop, finishing August at 2.35 percent, down 23 basis points. Lower rates mean higher bond prices, and the Barclays Capital Aggregate Bond Index gained 1.10 percent in August.

August revisions show U.S. economy growing even faster

Economic reports in August continued strong but showed some soft pockets. Good news included second-quarter gross domestic product growth, which was revised upward to 4.2 percent; consumer confidence, which recovered to a seven-year high; and business confidence. Housing starts rebounded sharply after weakness in July, while prices continued to increase.

Personal spending, however, declined for the month, and on the business side, industrial production was disappointing.

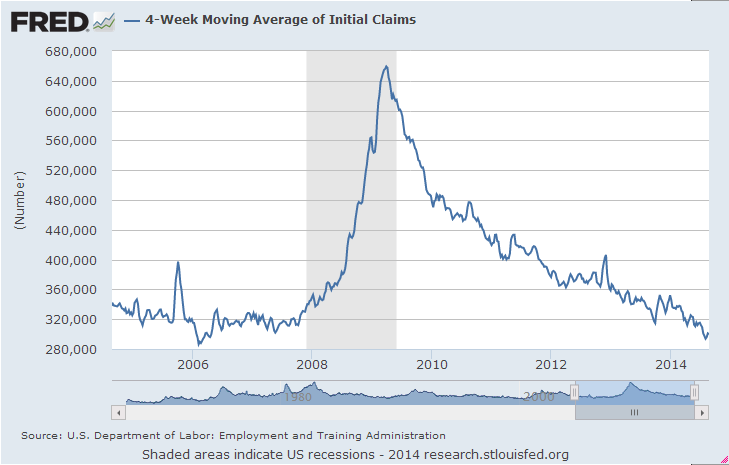

Employment growth remained strong. Initial jobless claims remained under 300,000, a sign of strength. The four-week moving average also remained below 300,000 for much of the month, which last occurred before the recession (see chart). The unemployment rate rose slightly, also a sign of strength because the recovering economy has lured more people back into the labor market.

The big economic news for August was Janet Yellen’s speech at the Federal Reserve’s (Fed) annual Jackson Hole Economic Policy Symposium. She noted that, overall, the domestic economy was growing faster than the Fed had expected and the labor market was improving more quickly. But she cautioned that risks remained and that the Fed intended to continue its stimulative policy bias.

International risks return to the forefront

As the U.S. economy grew, European growth slowed further. The German economy shrank 0.2 percent in the second quarter, and other European countries also had problems. Further worsening the situation is the growing crisis in Ukraine.

Other hotspots, like Syria and Iraq, continue to simmer due to the ISIS insurgency. The Israeli/Gaza conflict also remains on the table. Finally, although China’s growth has recovered, questions about the sustainability of its growth model remain.

A beautiful August could lead to a beautiful fall

After a difficult first half of the year, the U.S. summer has been much better. Fundamentals remain very strong, suggesting that the sunshine will continue.

Even so, we can see storms forming around the world. Europe remains politically and economically fraught, with the ECB preparing to implement policies that it had once categorically ruled out. Iraq and Syria continue to devolve into warlord-led violence, as does Libya.

The U.S. has largely benefited from these trends but may not continue to do so if they worsen. Even as the Fed ratifies the U.S. recovery by preparing to end its bond purchases, a crisis in Europe or Asia could easily shock our economy. U.S. markets are priced for the good news to continue, so any sign that it will not could have a disproportionate effect.

Still, the U.S. remains the most politically stable and economically solid of the major economies. Any short-term volatility may rock the boat but no more than that. As always, a properly constructed portfolio can give good returns in good times and a solid framework in bad times, regardless of sunshine or stormy weather.

All information according to Bloomberg, unless stated otherwise.

Disclosure: Certain sections of this commentary contain forward-looking statements that are based on our reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. Past performance is not indicative of future results. Diversification does not assure a profit or protect against loss in declining markets. All indices are unmanaged and investors cannot invest directly into an index. The S&P 500 Index is a broad-based measurement of changes in stock market conditions based on the average performance of 500 widely held common stocks. The Dow Jones Industrial Average is a price-weighted average of 30 actively traded blue-chip stocks. The Nasdaq Composite Index measures the performance of all issues listed in the Nasdaq Stock Market, except for rights, warrants, units, and convertible debentures. The MSCI EAFE Index is a float-adjusted market capitalization index designed to measure developed market equity performance, excluding the U.S. and Canada. The MSCI Emerging Markets Index is a market capitalization-weighted index composed of companies representative of the market structure of 26 emerging market countries in Europe, Latin America, and the Pacific Basin. It excludes closed markets and those shares in otherwise free markets that are not purchasable by foreigners. The Barclays Capital Aggregate Bond Index is an unmanaged market value-weighted index representing securities that are SEC-registered, taxable, and dollar-denominated. It covers the U.S. investment-grade fixed-rate bond market, with index components for a combination of the Barclays Capital government and corporate securities, mortgage-backed pass-through securities, and asset-backed securities.

###

Manning Wealth Management is a financial advisor and consultant office located at 2550 5th Ave Suite 800 San Diego, CA 92103. They offer securities and advisory services as an Investment Adviser Representative of Commonwealth Financial Network®, Member FINRA/SIPC, a Registered Investment Adviser. They can be reached at 619-237-9977 or at www.manningwm.com

Authored by the Investment Research team at Commonwealth Financial Network.

© 2014 Commonwealth Financial Network®