To avoid what I consider to be an unnecessary increase in my taxes, I will vote no on Proposition E: Coronado Unified School District $29 Million Bond Measure. My decision to vote “no” is based on the following considerations:

- I cannot get past the fiasco of the Brian Bent Memorial Aquatics Complex (BBMAC) and the concerns that it creates about the ability of the school district to manage competently its resources, in particular, the $29 million in additional revenue that it would receive if Proposition E is approved.

- I am not convinced that the school district cannot resolve its financial issues by selling the 2.2-acre site of the former Glorietta School, exploiting additional opportunities to charge for its programs and services, and by making some of the cuts that are described in the school district’s paper “Efficiencies for the 14-15 School Year: Continuing Considerations of Options” that can be found on the school district’s website. Many of these cost savings could be achieved without significantly detracting from the quality of the education provided by the schools. (It is my understanding that the school district has not made a final decision on the cuts that it would make in the event that Proposition E does not pass. The paper cited above is the only comprehensive description of potential cuts that I have been able to find.)

- I believe approval of Proposition E only serves to reward the State of California for its wasteful spending and costly policies and will only encourage the future waste of billions of the tax revenue that the state collects annually.

- Structuring the proposition as approval of a facilities bond rather than a parcel tax, thereby requiring only a 55 percent majority rather than the two-thirds supermajority required to enact a parcel tax, takes advantage of a change in California’s constitution that undermined the protection from increases in property taxes contained in Proposition 13 and could lead to unnecessary expenditures, while not freeing funds to pay operating costs.

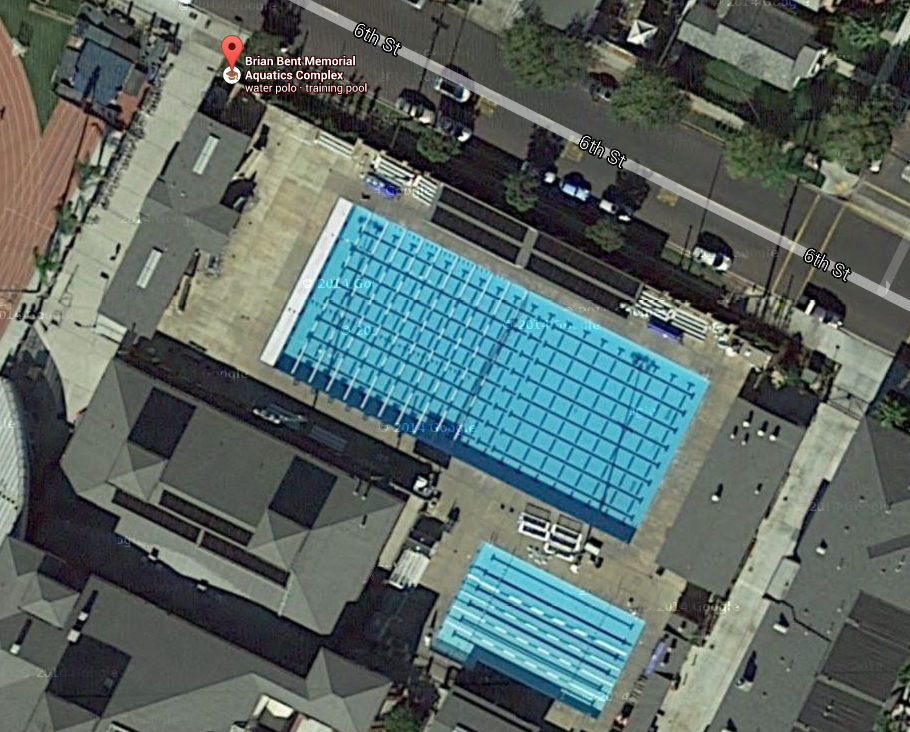

The Brian Bent Memorial Aquatics Complex

The BBMAC is an unnecessary extravagance that came about because of the failure of the school district to exercise adequate due diligence. (It is worth noting that at the time only one high school in the San Diego Unified School District, La Jolla High School, had a pool, and it was built with private money.) Further, the history of the BBMAC and present representations about its financial circumstances raise questions about the candor of the school district and its ability to manage its finances. Historically, the school’s swim and water polo teams used the city’s municipal pool, which was made available to the teams for free. Despite the long history of using the municipal pool, the school district paid more than $4 million, approximately $500,000 of which needed to be borrowed, to build a redundant facility. (I am confident that the school district could have continued to use the municipal pool at no or a modest cost. If this was not possible I would welcome an explanation of why.)

The BBMAC is an unnecessary extravagance that came about because of the failure of the school district to exercise adequate due diligence. (It is worth noting that at the time only one high school in the San Diego Unified School District, La Jolla High School, had a pool, and it was built with private money.) Further, the history of the BBMAC and present representations about its financial circumstances raise questions about the candor of the school district and its ability to manage its finances. Historically, the school’s swim and water polo teams used the city’s municipal pool, which was made available to the teams for free. Despite the long history of using the municipal pool, the school district paid more than $4 million, approximately $500,000 of which needed to be borrowed, to build a redundant facility. (I am confident that the school district could have continued to use the municipal pool at no or a modest cost. If this was not possible I would welcome an explanation of why.)

The operating costs of the BBMAC, which were grossly underestimated, were supposed to be paid by a private foundation with no contribution from the school’s general fund. The foundation and a successor foundation almost immediately defaulted on this obligation. As a result the school district has contributed almost $100,000 per year in fiscal years 2009-2010 through 2012-2013, a total of approximately $400,000, to help cover the operating losses of the BBMAC. Further, according to the Coronado Unified School District Three Year Projected Budget Comparison the school district will contribute an additional $100,000 in fiscal year 2013-2014 to offset a portion of the pool’s operating losses. An explanation of the rationale for these payments is that they offset the costs that the school district would have incurred to rent pool time elsewhere. This rational is difficult to accept based on the history of having used the municipal pool for free. Another school district document states that the BBMAC has allowed the school to avoid $170,000 in fees for the rental of other pool facilities. This statement also ignores the previous history of using the municipal pool. Further, it is not clear how to reconcile this statement with the approximately $400,000 that has been paid for the use of the BBMAC by the school’s sports teams.

The website that is promoting the bond measure states that “the District has carefully tailored and managed the facility’s operations over the course of the last few years, and by doing so it has eliminated any negative consequences to CUSD. In fact, this year the aquatics facility will run at a modest profit to the District with zero encroachment upon the District’s other funds.” The district’s website makes a similar statement “Actually the BBMAC almost made money in 12-13 and in 13-14 it is expected to become profitable.” I cannot reconcile the foregoing statements with school district data that indicates that the district contributed $99,661 in FY 2012-13 and is projected to contribute an additional $99,661 in 2013-14 to offset operating losses by the pool. Further, both statements totally ignore the annual debt service on the funds that were borrowed to build the pool. I believe that the more accurate assessment of the fiscal impact of the BBMAC on the school district was conveyed in the school Superintendent’s statement on April 12, 2010 in which he stated, “In addition, I must be bluntly truthful and say that the pool will always be a cost to the District any hope of profit will always be discouraged by other unexpected expenses ” One of these unexpected expenses is the $60,000 that the school district will have to pay to repair the pool deck, if it is unsuccessful in its claim against the contractor for a construction defect.

Adding insult to injury, the pool is used very little by the school district because of the need to rent it to outside organizations to offset its almost $500,000 in annual operating costs. The lion’s share of the BBMAC’s revenue, almost 85 % of its revenue in FY 2010-11 and FY 2011-12, was the result of its rental to these organizations. Absent this income, the operating losses of the BBMAC would increase dramatically.

Glorietta School Site, Other Potential Revenue Sources and Savings Opportunities

I am also not convinced that the school district has not overlooked other sources of revenue that could solve its budget issues. The school district owns the 2.2 acre former site of Glorietta School at Second Street and Prospect Place. The site is presently occupied by Villa Coronado, which pays the school district $20,000 a month in lease payments. Based on property values in Coronado, this site could be worth more than $11 million. (In 2005 the land occupied by the Middle School was estimated to be worth $5 million an acre.)

It has been explained to me by a member of the school board that selling the site would deprive the school district of a long-term asset and the sale of the site should not be used to pay current costs. This is a judgment. Since I believe that California’s taxes are already high enough and much of the tax revenue is wasted, as explained below, I would opt to sell the real estate before asking residents to pay more in taxes.

On its webpage, Coronadousd.net, under Frequently Asked Questions, the school district explains that the proceeds from the sale of this property could be restricted to paying for construction and modernization. While restrictions on the use of funds can limit flexibility in their use, construction and modernization sounds very much like the proposed uses of the funds that would be generated by the bonds sold under Proposition E, e.g., upgrading fire alarms; adding sprinklers, fire safety doors, and security systems including lighting and fences; installing energy efficient systems; and improving HVAC and lighting systems. Further, the proceeds from the sale of bonds under Proposition E would be used to refinance the school’s lease purchase obligations that were used to finance the construction of the schools’ facilities, which were clearly capital expenditures, and therefore would be a potentially legitimate use of the proceeds of sale of the Glorietta School property.

Further, while there are restrictions on the ability for the school to charge for its programs and services, I am not convinced that the school district is charging for all the services that it could and where it is charging, whether it is charging enough. For example, the school district charges $330/month for three year olds to attend its half day preschool program for three days a week. By comparison the Sandpiper School in Coronado charges $560-571 a month for its comparable program. Another example is what the Coronado school district charges for participation five days a week in its before school program for grades K through 7th, which is $90/month. By comparison, the same public school program in Fairfax, Virginia costs as much $154/month. Similarly, Fairfax charges more for its after school program.

I recognize that not all of the families of the school district’s students have the means to pay increased fees, although many of them do. I have also been told that California law precludes using “means tests” in assessing the costs of school programs. In order to address the potential hardship of increased fees, the school foundation could develop a privately funded scholarship program for less affluent students.

Finally, many of the potential cost savings identified in the paper “Efficiencies for the 14-15 School Year: Continuing Considerations of Options” would not significantly detract from the quality of education in Coronado’s public schools. Overall, the paper identifies $2,639,069 in potential savings. If the Glorietta property were sold it would eliminate the need to make all of these cuts. Further, it is unclear that it will be necessary to achieve $2.6 million in savings. I have been provided with a projection of the estimated revenues in 2014-2015 that indicates the district will receive $28.6 million in revenue and incur $30.5 million in expenses. This indicates that the shortfall is potentially closer to $1.9 million.

A total of $406,927 in potential savings has been identified for the Village Elementary School. Of this amount $256,687 or 63 percent would result from eliminating the equivalent of approximately three teaching positions by incorporating instruction in music, science labs, art, literacy and English Language Development (ELD) into the regular class room under the guidance of teachers with multiple credentials qualified to teach all subjects within the elementary classroom. Students would still receive instruction in these areas, just not by a specialized teacher. While this may not be ideal, I do not believe that it would be “devastating” to the quality of the education provided to the students. The balance of the potential savings, $150,240 would involve reductions in front office clerical support, staff support to the physical education and ELD programs, and the part time availability of a counselor. Again, these staff reductions should not materially detract from the quality of the elementary education.

Of the $151,481 in potential savings that have been identified for the Silver Strand Elementary School, $52,931, or approximately 35 percent of the savings, would not directly impact the instruction of the students. They would consist of eliminating what appear to be a part time assistant principal position and part time counselor services.

Of the $201,431 in potential savings that have been identified for the Coronado Middle School, $81,431 or 40 percent would also not appear to detract significantly from the students’ education. The proposed savings include a small potential reduction ($5,643) in support of non-athletic extended day activities, e.g., Associated Student Body (ASB) activities, yearbook, band/choir, Junior Optimist, and Reading Club. Other proposed savings that would have limited implications to the quality of the education are reductions in front office clerical support and Campus Assistants.

A total of $449,097 in potential savings has been identified for the high school. This is another case of where a substantial percentage of the potential cuts, $269,097 or approximately 69 percent, would not dramatically impact the majority of the school’s students. Elimination of elective courses that have enrollments of fewer than 22 students would generate $165,000 in savings. Courses potentially eliminated would include Hip Hop Dance and Advanced Placement courses in music theory and Spanish literature and advanced woodworking. The remaining $104,097 in potential cuts include elimination of an ASB preparation period, reduction in counselor services, elimination of the taxes and benefits expenses for the Coronado TV Executive producer (the salary of this position is paid by the Coronado School of the Arts Foundation), and a reduction in clerical support and the services of an Assistant Athletic Trainer.

A recurring theme of the proposed cuts relate to reductions in the availability of counseling services. However, it is not clear that these cuts would be necessary. The city provided the school district with $319,550 for counseling services in 2013-2014. These funds were for the salary and benefits of the current part time elementary school counselor, the position that has been identified as a potential cost savings. They also provided the funds for a new full time elementary counselor, the salary and benefits for the part time middle school counselor, and the funds for a full time staff person for the school’s Coronado Response Group, which is essentially a counseling service. I am confident that the same level of funding will be sought by the school district for the 2014-2015 school year and, if requested, it will be approved by the City Council.

Other potential cuts that should not dramatically impact the education of the schools’ students include the elimination of the services of a Construction Accountant and a Print Shop Technician; increasing the replacement cycle for notebooks, laptops, and desktops; reducing travel and conference expenses for the Maintenance, Operations and Transportation staff; and discontinuing the district subsidy to the BBMAC. These potential savings add up to $285,161.

No potential savings have been identified for the Palm Academy, for which the district previously received from the state a financial incentive to maintain. I have been advised that the program is expensive and the district is not required to offer it. Although it has an enrollment of only 13 students in 2013-2014, Palm Academy requires the support of a half-time principal, one full time teacher, and one full time staff person. If it were eliminated the district would save between $85,000 and $150,000 per year. The Coronado School of the Arts (COSA) is another program that the school district is not required to provide and which costs the district approximately $170,000 per year. Its programs may offer additional opportunities for savings.

In summary, approximately $1.1 million of the potential savings identified in the paper the “Efficiencies for the 14-15 School Year: Continuing Considerations of Options” could be made without dramatically impacting the quality of the education offered by the public schools in Coronado. Eliminating the Palm Academy could increase these savings by an additional $85,000 to $150,000 and changes in the program offered by COSA could result in additional savings.

California’s Wasteful Spending and Costly Policies

In 2013 California had the highest state sales tax rate in the country at 7.5% and the eighth highest combined state and local sales tax rate at 8.41%. It also has the highest income tax rate bracket of any state at 12.3% (13.3% for incomes over $1 million) with the fourth highest average income tax rate at 7.13%. Overall, in 2011 California collected $4,914 per capita in state and local taxes placing it among the states with the highest state and local tax revenues in the country.

While it collects substantial tax revenue, California wastes millions. For example, after spending $500 million on a computer system to link the state’s 58 county circuit courts, the effort was abandoned. Similarly, the state incurred $250 million in cost overruns and four years of delays before it abandoned an effort to upgrade its payroll system. The state spent $15 million to build ten hydrogen fueling stations even though there are only a couple of hundred hydrogen powered cars in the state.

In addition to wasting funds, the state has failed to take advantage of opportunities to receive additional funding. It missed out on $516 million because it failed to take advantage of a new Federal program. The California Employment Development Department could have received these funds, if it had invested in computer modifications that would have allowed it to recover the overpayment of unemployment benefits.

Another dimension of the failings of California is its performance in attracting and retaining business, which in turn would generate more revenue for the state and its schools. California is routinely voted as one of the most business unfriendly states in the country. In 2007 it was ranked 47th in “business-friendliness” and in 2009 it was 48th. It was also 48th in its business tax climate. In a 2013 small business survey the state received an overall grade of “D” with a grade “F” in the friendliness to business of its health and safety; employment, labor and hiring; tax code and tax related; and environmental regulations. In a 2013 survey of CEOs, California was ranked last in business friendliness. The latest casualty of California’s business unfriendly laws and polices is Toyota, which will move its 3,000+ headquarters jobs to Texas. Toyota follows Nissan, which moved its headquarters to Nashville in 2008. When Nissan moved, 68 percent of its workers decided not to follow the company. A consequence of California’s disdain for business was its 8.1 percent unemployment rate in March 2014, making it the state with the fourth highest unemployment rate.

Some key quotations from CEOs included, “California is getting worse, if that is even possible” and “I am not aware of any businesses other than entertainment that will be expanding or moving into CA. It is a black hole.” Another insightful quotation was “Only they [California has] going for them is the immigrant influx and the established industries already there.” This quotation highlights the issue of illegal immigrants on California’s educational system. The Pew Hispanic Center reported that as of 2008, 13.5% of the state’s K-12 students were the children of illegal immigrants. The cost of educating these students was $10.8 billion out of a total education budget of $72 billion or 15 percent of the budget.

While the issue of illegal immigration is largely the concern of the Federal government, California has taken steps that further exacerbate the problem. (Whether you agree or disagree with the laws regarding the treatment of illegal immigrants, California’s first obligation should be to protect the interests of it legal residents, and it should not enact laws or embrace policies that are detrimental to them, e.g., cause additional resources to be expended on educating the children of illegal immigrants.)

In 2011 it passed a law that prohibits the state, cities and counties from mandating employers to use the Federal E-Verify system or face the loss of their business licenses. (The E-Verify system uses Federal data bases to check the immigration status of workers.) The recently passed Trust Act in California bars police from cooperating with Immigration and Customs Enforcement (ICE) officers. Under the law, local police are not required to honor ICE requests to detain suspects who are in the country illegally who have committed certain offenses. Since California accounts for almost one-third of the deportations from the United States, the Trust Act has the potential to reduce significantly the number of deportations thereby possibly increasing the number of illegal immigrant school children.

To put it in perspective, in 2010 California was ranked eleventh in state and local taxes collected per capita but it was 37th in state and local preK-12 per-pupil funding. This was the largest disparity of any state and contrary to most other states, where there was almost a direct correlation between state and local tax revenue per capita and how much was spent per student. For example, Connecticut was ranked fourth in per capita state and local taxes collected and fourth in its funding per student. By another measure, the ratio of spending per student to state and local tax revenues per capita, California fared even worse. It was ranked 49th . In 2010 state and local funding per pupil was $8,999 and its per capita state and local tax revenues were $4,623. (The state with the highest ratio was New Hampshire, which provided $13,282 in preK-12 funding per student and received $3,812 per capita in state and local taxes.) California’s dismal performance begs the questions of its commitment to education and where the revenue is going.

Parcel Tax Versus a School Bond

For 121 years prior to the passage of Proposition 39 in 2000, the state constitution required a 66.7 percent majority to approve local bonds paid for exclusively by property owners. Proposition 39 reduced the required majority to 55 percent for local school bonds. However, parcel taxes continue to require a 66.7 percent supermajority for passage.

According to the California State PTA “By law, local school districts are allowed to raise funds for school programs only through parcel taxes.” Proposition 13 allowed school districts to raise local funds through school facility bonds (for school facilities only) and school parcel taxes. Until the passage of Proposition 39 both school facilities bonds and parcel taxes required a 66.7 percent supermajority to pass. Proposition 39 reduced the requirement for school facilities bonds by allowing them to be adopted by a 55 percent majority vote, but it did not change the 66.7 supermajority required to pass a parcel tax.

Specifically, Proposition 39 amended the state’s constitution to allow bonds to be approved by a 55 percent majority for “the construction, reconstruction, rehabilitation or replacement of school facilities including the furnishing and equipping of school facilities.” The changes in the constitution do not explicitly permit the bonds to fund “repairs” although the description of the intent of the proposition does indicate its purpose was to allow the bonds to be used for the “repairing, building, furnishing and equipping of school facilities.” The changes in the constitution also require voters to be provided with “a list of specific school facility projects to be funded and certification that the school district board, community college board, or county office of education has evaluated safety, class size reduction, and information technology needs in developing the list.”

In my estimation the school district has not provided a specific list of projects. Instead the text of the measure that will appear on the ballot provides a list of illustrative projects, e.g., to upgrade and install security systems such as security lighting, fencing, smoke detectors, and fire alarms and sprinklers for improved student safety. It goes on to include a “laundry list” of virtually every conceivable facilities and IT related project including the acquisition and upgrading of automobiles. It also includes by reference a Facility Master Plan. While this may satisfy the legal requirement to provide a specific list, in my estimation it is essentially a “blank check” to undertake any facilities or IT project regardless of its necessity or merit. My opinion of the lack of specificity of the list provided by the school district is reinforced by the district’s Memo re: G.O. Bond proceeds expenditures and effect on the General Fund, which states “The project list is intended to allow project needs to change as facility/IT needs change in the future.”

In its fact sheet on Proposition E, the school district states that the proceeds from the bonds would free General Fund and Fund 40 dollars leading to smaller class sizes and advanced programs in math, science, and technology. This presupposes that absent the proceeds from the bonds, the school district will spend $29 million over the next ten years on facilities and IT projects that are truly required to achieve the school district’s goals of funding advanced programs in math, science, and technology; maintaining manageable class sizes; providing the facilities and equipment needed for career and technical education; and keeping school facilities clean and well maintained. If the bona fide needs for facilities and IT projects are less, then the General Fund and Fund 40 would not make investments of this magnitude and the benefit of the bond proceeds would be reduced.

In the above referenced memo the school district provides information on its facility maintenance and repair and IT expenses in 2013-2014 that would have been appropriate uses of bond proceeds. Specific expenditures included repairs to the schools’ windows, bleachers, elevators, fences, and bathroom tile despite the fact that the school buildings are relatively new. Other expenses included replacement of the drinking fountains in the Village Elementary School, an exterior crown preschool logo, installation of artificial turf on the field shared by the high and elementary schools, and installation of skateboard racks at Village Elementary.

The nature of the projects undertaken by the school district in 2013-2014 that would have been eligible for bond funding raises two questions. First, many of them are simple repairs that are no more than routine maintenance. I feel considering these to be legitimate projects for bond funding is an overly liberal interpretation of what kinds of projects are allowed to be funded by bond proceeds. As noted above, the revised language in the state constitution does not include “repairs.” While repairs may have been funded in bonds previously approved pursuant to Proposition 39, the inclusion of this type of work further erodes the protections against property tax increases provided in Proposition 13. The second question is whether the school district can be trusted to spend judiciously an additional $29 million in revenue, after it decided to proceed with projects such as the installation of an exterior logo at the preschool and skateboard racks at the Village Elementary, while it was contending with a tight budget.

My concern is that over the next 10 years there will not be $29 million in truly required facilities and IT projects. If Proposition E is passed, the bond funds will be consumed by “nice to have” projects. (The decision to construct the BBMAC was driven by special interests. The availability of $29 million in additional revenue will spawn a host of other persuasive special interests with plans for how this money should be spent. The money will be spent regardless of whatever oversight and safeguards are promised.) The General Fund and Fund 40 will not realize any savings because they will not have been budgeted to pay for this work. (Savings will only be realized if the funds are budgeted and then not required through the use of bond proceeds.) The eventual outcome could be the need for a parcel tax to supplement the funds available to satisfy the school district’s increasing appetite for resources. (In the seven years from 2007-2008 to 2013-2014 the school’s expenditures increased by almost 16 percent.) At the same time the residents of Coronado would have paid, through an increase in their property taxes, for facilities and IT projects that were not truly required.

In conclusion, based on its history with the BBMAC, the school district cannot be trusted with up to $29 million in additional bond proceeds. It needs to generate additional revenue from existing sources and assets and make the cuts that are required to live within its means. It should be able to do this without significantly detracting from the quality of the education offered by the city’s public schools. Further, the residents of California are already heavily taxed, affording the state substantial tax revenues. However the state is wasteful and inefficient in its spending, does little to be competitive nationally, and enacts laws that further increase its costs. Levying additional