Often the summer can be a lazy time for the markets, with many executives and traders on vacation around the world. Not this year. There’s a lot going on in the summer of 2015.

U.S. and international equity markets around the world have weakened in recent weeks, driven primarily by three factors:

- Stock market plunge and currency devaluation in China

- Weak 2nd Quarter corporate earnings in the U.S.

- Looming Federal Reserve Interest Rate Hike

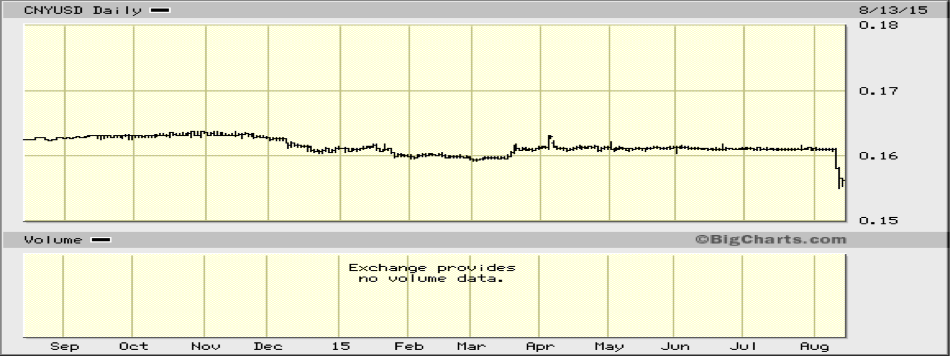

Currency Devaluation in China

First, by far the most important issue in the global markets in recent weeks has been the situation in China. (Greece was top of mind last quarter, but it has been eclipsed. I discussed the Greek debt problem in my 2Q update here, and will not re-address in this note.)

China’s growth is slowing, and this has important ramifications for global markets. China has the world’s second largest economy, but because it has been growing so fast in recent years it has contributed more to global economic growth than any other country. Now that growth is slowing. In order to try to protect its economy, the Chinese government has resorted to propping up its stock market with government funds and, this week, announcing a surprise devaluation of its currency, the yuan. August 11th‘s 1.9% drop in the yuan relative to the dollar was the biggest one-day decline since 1994. (The Chinese government fixes the value of the yuan relative to the dollar by specifying a band in which it can trade.)

The intended effect of this devaluation is to protect the Chinese economy by making Chinese exports cheaper for foreigners to buy. The Chinese government systematically reports GDP growth of about 7% (its own target), but these figures are highly suspect and most global investors believe growth has slowed well below this figure. But perhaps the most important signal sent by the devaluation is a whiff of panic from the Chinese government that they do not have a handle on how best to cope with the slowdown. Normally the government keeps the yuan steady through crises, even as it neighbors are devaluing their currencies.

Credit: BigCharts. One-year chart of yuan to USD. Note the big drops in August.

Weak U.S. Corporate Earnings

The second reason for market weakness is that U.S corporate earnings for the second quarter have been relatively uninspiring. Our large multinationals are contending with a strong dollar, which make their foreign currency profits add up to fewer dollars and it makes their products relatively more costly than competitor products priced in euros or yen. The dollar has made a very strong run over recent years and has held its ground most of this year.

Credit: BigCharts. One-year chart of Dollar Index (DXY)

Interest Rate Hike

Third, investors are wary that the first rate hike by the Federal Reserve will come in September despite the weak global (but not U.S.) economic data. While the labor market here in the U.S. continues to firm and consumer spending is resilient (due in large part to lower energy prices), commodity prices are declining, thus introducing a deflationary element into the economic equation. Investors are worried that the Fed will overlook these worries and tighten policy by 25 basis points anyway at its September meeting.

The bottom line is that U.S. stocks continue to trade at above-average valuations and don’t really need any excuse to go sideways for a while. Investors would be prudent to keep their expectations modest for the near future.

To learn more about how we structure client portfolios, please visit us at www.orionportfolios.com.

Peter C.Thoms, CFA