2014 Midyear Update

Economic Growth Resuming, Markets Rangebound

Presented by Michael Manning

The initial outlook for 2014 was based on an improving economy across the board. As we approach the middle of the year, despite a weather-weakened first quarter, those expectations are playing out.

- After a slow first quarter, economic growth should heat back up to between 3 percent and 4 percent for the remainder of the year.

- Continued growth should have the Federal Reserve (Fed) completing the tapering process by the end of the year.

- Employment and wage growth should continue to accelerate.

- Earnings growth will have trouble meeting expectations, as rising wage bills and slowing productivity hit profit margins.

- Equity market growth will be constrained by earnings weakness, with the market trading around current levels for the remainder of the year.

“Snowdown” turns to meltup

We started 2014 in a much better place than we did 2013. Employment, both current and trend, was much better. The housing market was much improved. The consumer was much stronger. The government was much more stableand in a much better fiscal position. The stock market responded to this ongoing improvement by posting its best year since 1997.

Although the first quarter of the year was snowed out (hence the above moniker), the second quarter looks to fare much better, and there is the prospect of economic warming kicking in at the global level for the rest of the year. First-quarter economic growth of 0.1 percentwhich is quite likely to be revised to a losswas driven by record-setting snowstorms, leaving hundreds of thousands more workers than usual stuck at home in January and February. Improving weather in March and April sent those workers back in, along with many others, leading job figures to increase at their highest level in years and driving private employment to an all-time high.

As we look further into 2014, we can expect the underlying economic trends to continue. Growth in jobs has stabilized at around 200,000 per month, bringing unemployment down from 6.7 percent at the end of 2013 to 6.3 percent at the end of April 2014. House prices have continued to appreciate, and although the market appears to have slowed, it continues to improve. Business investment has remained at levels above those of recent years, while government spending and hiring has ceased to be a drag on the economy.

All things considered, I expect to see real economic growth of around 3 percent for the remainder of the year, with the possibility of stronger performance. With consumer spending growing at around 4 percent on a nominal basis, business investment growing at around 8 percent, and government spending essentially flat, 3 percent appears both reasonable and achievable. Combined with inflation of around 1.5 percent for the year, nominal growth should approach 4.5 percentbetter than we have seen for some time.

The risks here are largely on the upside. If consumer borrowing were to pick up, spending could grow faster than wage growth. Business investment could finally respond to improving demand and rise more than expected. Local and state governments could increase investment and hiring more than expected.

Downside risks are more limited and primarily external, with Europe and China remaining as possible negative actors in the world economy and financial markets. The major domestic downside risk is of slowing employment growth, of which there are few signs. Should employment growth drop, the rest of the economy would also slow. Nonetheless, the most probable case remains continued economic expansion.

The stock market, on the other hand, will face larger challenges this year and may struggle. I expect the U.S. equity markets to end 2014 at about the same level as they are nowaround 1,875 for the S&P 500. Although earnings will continue to grow, they will do so more slowly than expected, and valuations may be adjusted over the year as investors expect lower future growthand accordingly pay less for stocks. That willingness to pay less will also come because interest rates will rise somewhat over the year, making bonds more attractive as an investment and lowering the present value of the slowly growing earnings stream even more. The lower valuations will offset the somewhat higher earnings, leaving the market essentially flat for the year.

Unlike the economy, I believe the risks to the market are mostly on the downside. Valuations remain at high levelshigher on some metrics than they were in 2007, for example. Profit margins are at historic highs, and the tailwinds that got them there are disappearing. Stock buybacks, which have been responsible for much of the growth in earnings per share, appear to have peakedand, in any event, have become less effective for every dollar spent as prices increase. And unlike in the real economy, market-related debt has increased back to 2007 levels and above.

That said, there is also the possibility that retail investors could start to buy in to the marketwhich could drive prices even higher. This could be considered a “bubble effect” and would drive valuations even farther above historic norms. Although this could certainly happen in 2014, it would only set the stage for a more severe adjustment later on.

The following commentary will consider the economy and the markets separately; although they are linked, they behave very differentlyas we have seen over the past couple of yearsand respond very differently to the underlying supply and demand factors. We will look at the economy first and then examine the financial markets in light of our economic conclusions.

The Economy at Mid-2014

To better understand the economy, we can break it down into its four componentsconsumer spending, business investment, government spending and investment, and net exportsand examine each individually. For each component, we will look at real growth and then add in expected inflation, checking our conclusions against forecasts from other analysts. This process will help us understand where we can expect growth to come from and why.

Consumer spending

Representing about 70 percent of the economy as a whole, consumer spending is the single most important determinant of growth. It is composed of wage income, transfer income, investment income, and borrowing. Wages are the largest component of income, at just less than two-thirds, and the only income source for most families. Wages are also the most variable source of income.

Growth in wage income depends on three things: (1) growth in the number of jobs, (2) hours worked at each job, and (3) average pay for each hour worked. In other words, even if the number of jobs remains the same, if each worker works longer hours and/or wages per hour increase, wage income can rise.

At the end of 2013, we noted that the number of jobs had been increasing at a rate of between 1.5 percent and 1.75 percent per year for the past three years. So far in 2014, that trend has continued. Even in the weakest part of the first quarter, the job growth rate remained above the level of the same period in 2013, as well as much of 2012.

We can see the same trend for average hours worked in 2013 and into 2014. Although the first quarter showed a dip, we have recovered back to 2013 levels.

Finally, looking at the growth of the average hourly wage, we see that it continues to increase at a rate consistent with that of 2013, although the most recent report shows a small drop-off.

With all of these factors combined, wage income growth has averaged around 4 percent per year for the first part of 2014, with weakness in the first quarter offset by stronger growth both before and after. The chart below only shows private employment, so the effective growth rate would be somewhat below 4 percent.

Looking at actual growth in consumer spending, as compared with growth in private wage income, we see that spending has been accelerating since early 2013, a trend that continued into early 2014.

Initially, we estimated growth in consumer spending of about 3 percent for 2014. The fact that spending growth hit the 3-percent level in the first quarter, despite the weather effect, suggests that growth will be stronger as the economy continues to improve. All things considered, we have revised our estimate up to an expected growth rate of around 4 percent on a nominal basis for the remainder of 2014.

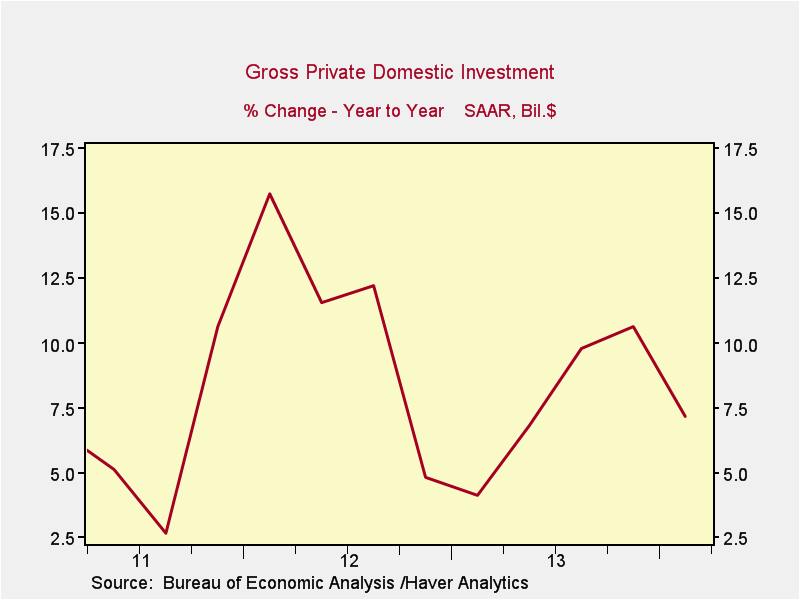

Business investment

Unlike consumer spending, business investment has not shown consistent growth. As the chart below illustrates, it has bounced around much more and has not yet achieved the consistent levels of the mid-2000s.

That said, despite first-quarter weakness as 2014 began, it appeared that business investment growth was normalizing around the 8-percent to 10-percent level of the mid-2000s, which is also consistent with the post-dot-com bubble experience.

At the start of the year, we expected business investment to grow at an annual rate of around 8 percent in 2014. This represents a return to normal levels, typical of the recovery periods after recessions. Sectors that should benefit include technology, construction (for investment in new facilities), and industrials. Year-to-date, there is no reason to revise that estimate. Although growth was somewhat slower in the first quarter, there are signals that it is picking up, and all of the initial arguments for higher levels from the start of the year remain effective.

Government spending

The question for 2014 growth is whether the change in government spending will continue to decline, return to positive levels, or hover around zero. At the start of the year, our expectation was that, despite the declines in 2013, overall government spending would return to a net-zero level through 2014. That appears to be what the data is now showing, and there is no reason to revise this estimate.

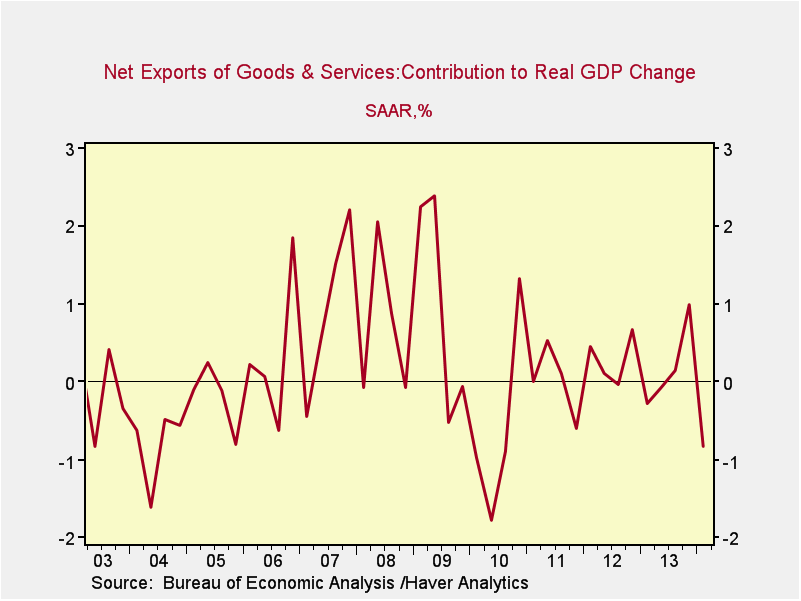

Net exports

The final component of the economy, net exports, will most likely continue to bounce around a zero contribution to gross domestic product (GDP) growth, as shown in the following chart.

Offsetting factors include a decline in petroleum imports, driven by the fracking oil and gas boom, and a probable increase in imports, driven by an improving economy and consumer spending. Overall, imports greatly exceed exports, creating a drag on growth, but this is unlikely to change in 2014. Despite the weak results from the first quarter, we continue to expect net exports to average around zero for the remainder of the year.

Conclusions

Taking into account the aggregate factors above, we should expect to see real growth increase by around 3 percent for the remainder of 2014, with growth accelerating over the course of the year. Given the weak first quarter, which may be revised down to reflect actual shrinkage of the economy, we expect growth for the year as a whole to be around 3 percent as well.

With inflation estimated at approximately 1.5 percent, this equates to nominal growth of around 4.5 percent. This is somewhat above the past several quarters and reflects the absence of drag from federal spending cuts, as well as the overall improvement in the economy. It is also consistent with the range predicted by a broad spectrum of forecasters.

This is a healthy growth rate, beginning to approach that of past recoveries, and it should result in accelerating growth in employment and wage income. Supporting forces include the moderating but ongoing housing recovery, relocation of manufacturing jobs to the U.S., slow recovery in the rest of the world, and normalization of government spending at all levels. Risk factors include potential relapses in China and Europe, as well as possible financial turbulence in the markets, which is the subject of the next section.

Financial Markets in Mid-2014

Fixed income

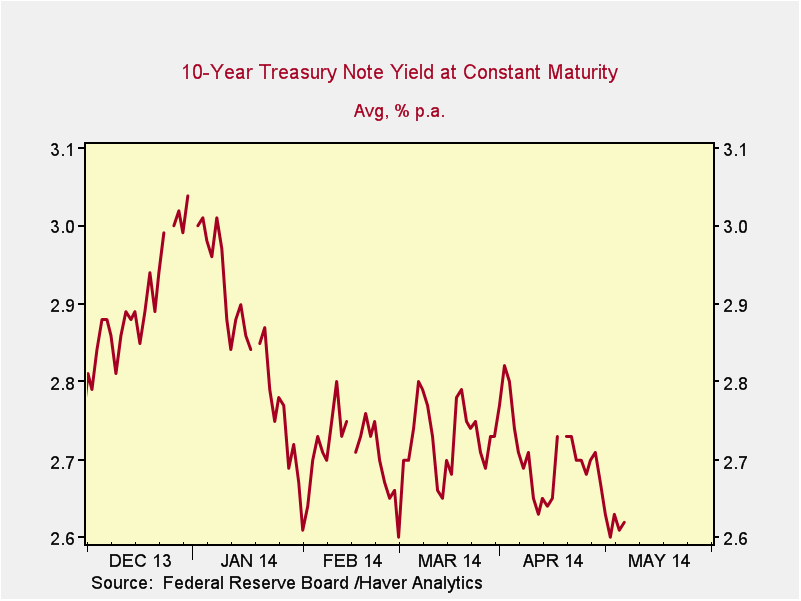

As 2013 ended, the Federal Reserve began to taper, or slowly reduce, the bond purchases it makes in order to stimulate the economy. In theory, the taper means two things: (1) the economy is improving and needs less support, in the Fed’s judgment; and (2) interest rates are likely to increase as the Fed exits the market. (Presumably, it has been buying at higher prices and lower rates than other market participants.)

Now nearing mid-2014, we find that, instead of increasing, rates have actually declined from the levels of 2013. Rates ranged from around 2.75 percent to 3 percent in the second half of 2013, with a tendency toward the upper end of the range; in 2014, rates have stayed between 2.6 percent and 2.8 percent, even as the taper has continued.

While I noted in my last update the reasons why rate increases might be limited, and that “2014 should include periods of both rising and falling rates,” the fact that rates have not only not increased but actually declined suggests that any increase will be more limited than I expected. At the same time, the fact that we are now closer to the end of the Fed’s interventionand the economy continues to acceleratesuggests that rates quite possibly will increase faster toward the end of the year than many forecasters currently expect.

I believe rates will remain near current levels for the next quarter or so, before moving upward as the Fed approaches the end of its policy of quantitative easing, growth continues to accelerate, and inflation starts to edge above the target rate, ending the year at around 3 percent to 3.5 percent for the 10-year U.S. Treasury bond.

This expected stability in current rates, with the possibility of a faster increase toward the end of the year, should result in fixed income risk rising over that time period. As a result, and because rates are still low by historical standards, focusing on credit, such as corporate bonds, should continue to provide incremental returns, even though spreads are at low levels.

The U.S. stock market

There are three key variables here: (1) the growth rate of the economy as a whole, which we discussed earlier and which will determine corporate revenue; (2) the level and change in profit margins, which, together with the overall economic growth rate, will determine corporate earnings growth; and (3) the level of price multiples (or how much investors will pay for a given level of earnings).

Corporate revenue. As stated above, I expect U.S. growth to be in the 4.5-percent range on a nominal basis for 2014. Much of this will come from growth in consumer spending, but business investment will also contribute significantly, and government is poised to stop subtracting from growth.

Aggregate corporate revenue (the top line) grows over time at the rate of GDP growth, so we can reasonably estimate revenue growth at, say, 4.5 percent. This may even be generous. As of May 9, the S&P 500 Index reported an overall revenue growth rate of 2.7 percent for the first quarter, according to FactSet. Although this rate was certainly affected by weather, it will act as a drag on the year as a whole. More than that, the sector reporting the highest growth in sales was utilities, supported by the gas industry, which actually benefited from the weather.

I expect to see revenue growth accelerate along with the recovery, but I see no reason at this point to adjust the 2014 estimate upward from the initial 4 percent, which seems reasonably fair but isn’t a slam dunk. Looking at the past couple of years, we can also see that revenue growth has exceeded 5 percent in only one of the last seven quarters. The averagearound 4 percentis consistent with expectations.

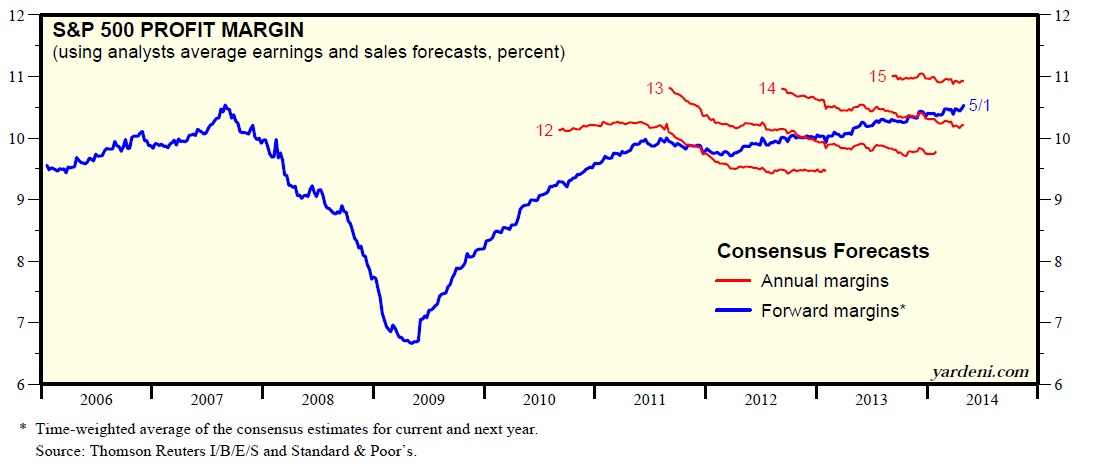

Profit margins. If nothing else changes, with revenue growth of 4 percent, we would also see corporate earnings grow at 4 percent, depending on how well the businesses are runthat is, on the profit margins. Profit margins are currently very close to all-time highs, which may limit any future improvements.

Current analyst estimates of margins for the next 12 months show improvement over 2014 levels, but I am not convinced of that. There are reasons to believe that margins might come downwith rising wages being the most prominentbut increasing operating leverage as the economy improves may well compensate for that.

A warning sign from the first-quarter earnings reporting season is that, per FactSet, 71 percent of companies, which is above average, have issued negative earnings guidance for the second quarter. This, combined with analyst expectations of earnings growth for the second through fourth quarters of 2014 of 6.1 percent, 9.8 percent, and 10.1 percent, respectively, suggests that a shortfall of actual performance versus expectations is quite possible.

Overall, margins can reasonably be expected to stay around current levels for 2014, so overall corporate earnings should grow by about 4 percent of the economy as a whole. The remaining question is: how much will investors be willing to pay for those earnings?

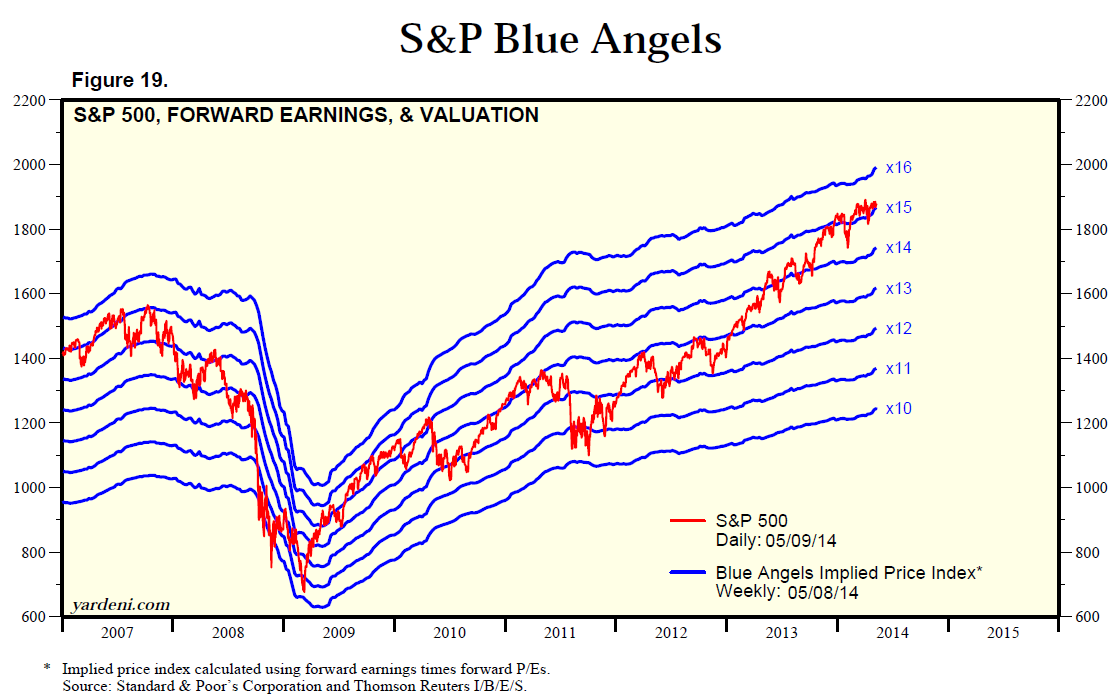

Price multiples. Looking at the past five years, multiples have bounced between 10x and 15x forward earnings for the S&P 500. Back at the peak in 2007, they even briefly exceeded 15x. My expectation at the start of the year was that it seemed unlikely that multiples would expand too much further in 2014. Year-to-date market results support this.

The market continues to trade around the 15x level on forward earnings, which is supported by the high growth expectations reported above. If, as expected, revenue and earnings growth come in below expectations, there is the possibility of a double adjustment in pricesfor lower earnings and with a lower multiple.

The Fed and the stock market. An additional supporting argument for the idea that valuations may tick down again comes from the actions of the Fed. The tapering process is well along, and the Fed is poised to stop its stimulative bond purchases altogether by year-end. As you can see in the following chart, the S&P 500 has largely followed the Fed’s bond purchasing program, and its cessation may have a negative effect on the market.

The end of the stimulus program should at least reduce the appreciation of the S&P 500, and, if the economy strengthens as I expect, the Fed may actually start raising short-term rates sooner than expected. Markets typically anticipate the Fed’s actions, and this will be another headwind.

Conclusions

Despite the weak first quarter (i.e., the snowdown), recent data shows that the recovery is intact and accelerative. If businesses continue to operate at their current very high profitability levels, the stock market can be expected to appreciate around 4 percent in 2014implying a year-end target of 1,880 for the S&P 500.

As of the middle of the year, this is consistent with market behavior. The question is whether earnings will continue to grow as expected while profit margins remain high. Upside risks include both fundamentals, with companies growing earnings faster than expected, and psychological indicators, with investors shifting to a more risk-tolerant mode and pushing multiples above 2007 levels.

In light of my conclusion that the economy is in a sustainable recovery, and that it also seems likely that margins should remain around current levels, valuations are the key variable. Valuations are typically based on the expected level of future growth, with investors willing to pay more for faster growth. As you can see from the above charts, expected future earnings growth (for the remainder of 2014 and 2015) looks quite high, and, even with strong economic growth, it could be tough to meet. If investors moderate their growth expectations, multiples could get hit.

Looking at the chart above, you can see that 14x forward earnings is a typical multiple for most of the past five years. Based on an earnings growth rate of around 4 percent, and using a 14x multiple, the indicated year-end target for the S&P 500 would be around 1,750.

Overall, I suspect that the risks to the economic growth rateand, therefore, for aggregate corporate earningsare on the upside, while margins and valuations are likely to decline slightly. The indicated target, then, is between the two indicators above: 1,750 and 1,880.

Looking at the market so far this year, we have cycled between 1,840 and 1,880 for most of that time. Although we’ve edged above that level recently, the momentum seems to have slowed.

With the Fed poised to end its stimulus in the next couple of months, with rates potentially rising into the end of the year, and with most metrics already about as favorable as they can get, I find the notion of continued double-digit appreciation hard to support. In fact, as mentioned above, I believe that the market will normalize in 2014. I am therefore projecting a year-end 2014 target of 1,875 for the S&P 500.

This is not a prediction of a flat, boring market. I believe a sell-off at some point this year is possible, as investors reexamine their holdings and process the end of the Fed’s stimulus program. I also expect investors to reassess the attractiveness of stocks as interest rates rise, which they may do during late 2014. Finally, I also expect wage growth to accelerate, which should have a negative effect on profit margins, even as it boosts the economy as a whole.

The risks for the market remain primarily on the downside for the remainder of 2014. Too many metrics are too highin many cases, at or above 2007 levels. This certainly doesn’t signal problems in the short term, but it probably does mean future appreciation opportunities are limited. It also does not take into account the possibilityindeed the likelihoodof unexpected negative events. As we saw with the weather in the first quarter, unexpected events can indeed hurt both the economy and the financial markets.

Wrapping It Up

Despite a weak first quarter, the recovery continues and should strengthen through the remainder of 2014. Interest rates have actually declined so far this year, but the end of Fed stimulusand the possibility of a sooner-than-expected rise in ratesshould result in moderate increases toward the end of the year.

As expected, financial markets have shown little appreciation so far this year, and they remain priced at high levels reflecting earnings expectations that will be difficult for companies to meet. Stocks are overvalued by many metrics, while many of the tailwinds that have sustained earnings growth are going away. Combining the effects of slower earnings growth with the potential for decreases in market multiples, I expect the market to close 2014 at around the same level at which it is right nowalthough the potential for a decline at some point during the year is very real.

Disclosures: Certain sections of this commentary contain forward-looking statements that are based on our reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. All indices are unmanaged and are not available for direct investment by the public. Past performance is not indicative of future results. Diversification does not assure a profit or protect against loss in declining markets. The S&P 500 is based on the average performance of the 500 industrial stocks monitored by Standard & Poor’s. Emerging market investments involve higher risks than investments from developed countries and also involve increased risks due to differences in accounting methods, foreign taxation, political instability, and currency fluctuation.

###

Manning Wealth Management is a financial advisor and consultant office located at 2550 5th Ave Suite 800 San Diego, CA 92103. They offer securities and advisory services as an Investment Adviser Representative of Commonwealth Financial Network®, Member FINRA/SIPC, a Registered Investment Adviser. They can be reached at 619-237-9977 or at www.manningwm.com.

Authored by Brad McMillan, CFA®, CAIA, MAI, AIF®, chief investment officer, at Commonwealth Financial Network.

© 2014 Commonwealth Financial Network®