Have You Outgrown Your SEP-IRA or Individual 401(k)?

By Peter C. Thoms, CFA

Founder, Orion Capital Management LLC

Check our our Tax Savings Analyzer and Defined Benefit Plan Fact Sheet

Markets, interest rates and future returns are uncertain. Investors need to take steps to ensure that they control the factors in their financial lives that they are able to control.

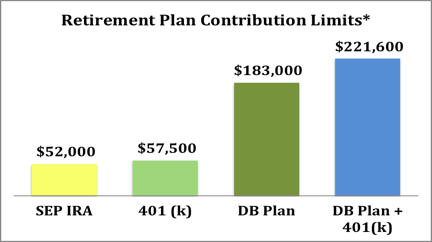

One such factor is choosing (and funding) the retirement plan that can best maximize tax savings. For high-income individuals who operate independently, there are basically three choices: a SEP-IRA, an Individual 401(k) and a defined benefit pension plan.

One of these plans is likely optimal for a given person’s situation. If the wrong plan is chosen, thousands of dollars in taxes will be needlessly paid out of your potential nest egg to the IRSeach year! It’s important to choose wisely.

Here are the contribution limits for 2014 for each type of plan.

*For a 52-year-old earning $300,000. 2014 plan maximum contribution limits include a “catch-up” contribution of $5,500 for 401(k).

Here are the main pros and cons of each type of plan. There’s obviously much more to each plan, but these are good starting points to consider.

SEP-IRA

SEP-IRA 2014 Contribution Limit: The lessor of $52,000 or 25% of income.

Pro: Takes 10 minutes to set up. Easy to administer.

Con: Because contributions are limited to 25% of income, someone with a lower income will not be able to come close to the $52,000 limit.

Individual 401(k)

Individual 401(k) 2014 Contribution Limit: Lessor of 100% of compensation or $52,000 ($57,500 if age 50 or older)

Pro: Good for owner-only businesses. In majority of cases will permit business owners to contribute a higher percentage of their income to the 401(k) than they would be able to with a SEP-IRA. For example, a real estate agent earning $100,000 will be able to make a higher tax-deferred contribution to an Individual 401(k) than to a SEP-IRA.

Con: Takes more paperwork to set up and administer and requires more detailed record keeping than a SEP-IRA.

Defined Benefit Plans (DB Plans)

DB Plan 2014 Contribution Limit: No single limit. The maximum contribution for each specific plan is determined by the business owner’s age, income, and years to retirement. For high earners, annual contribution limits can reach over $180,000 per year.

Pro: By far the highest potential tax-deferred contributions for high earnersexceeding even $200,000 per year for those in the right circumstances. Massive annual tax savings potential. Defined benefit plans enable the self-employed to build a large retirement nest egg in a very short amount of time. Plan owners can accumulate as much as $1,000,000 to $2,000,000 in a tax-deferred retirement account in just 5-10 years. Once a defined benefit plan is funded to the (approximate) IRS limit of $2.45 million, the plan assets can simply be rolled into a regular IRA.

Con: Set-up and annual administration is more costly than with a SEP-IRA or Individual 401(k). (These costs, however, will be more than offset by the resulting tax savings ) Also, defined benefit plans are much more of a commitment than the other two options above, which both have optional contributions.

Complimentary Tax Savings Analysis

If you are interested in learning how much you might be able to save in 2014 taxes by establishing a defined benefit plan before December 31, 2014, please visit us online using the link below. Just enter your information and we will generate a complimentary tax savings proposal for you and deliver it directly to your inbox.

Tax Savings Analyzer & Defined Benefit Plan Fact Sheet

Peter C. Thoms, CFA

Orion Capital Management LLC

1330 Orange Ave. Suite 302

Coronado, CA 92118

Tel: 619.435.1701

Email: [email protected]

Website: www.orionportfolios.com

About the Author:

Peter C. Thoms, CFA, is the founder and managing member of Orion Capital Management LLC, an independent Registered Investment Advisor based in Coronado, California. The firm focuses on managing global investment accounts for institutional and private clients.

Disclosure:

This document is for informational purposes only. Nothing in this report is to be construed as a specific investment recommendation. This document does not constitute the provision of investment advice, which is only provided by Orion Capital Management LLC under a written investment advisory agreement and only in states in which Orion Capital Management LLC is registered or is exempt from registration requirements. Orion is not a tax advisor and does not provide tax advice. For tax advice individuals should consult their CPA.